Vendor Portal

Vendor Portal

Author: Mark Ainely | Partner GC Realty & Development & Co-Host Straight Up Chicago Investor Podcast

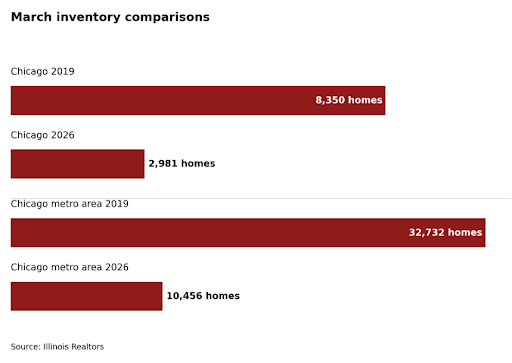

This weekend I was reading Crain's Chicago Business, yes the paper copy and not online, and I saw a chart that stopped me cold. It showed how low Chicago home inventory is right now compared to 2019. This did not happen overnight, but seeing the numbers laid out next to each other got me thinking about how this environment is shaping the way investors are investing in Chicagoland these days, or whether they are investing at all.

The numbers, published by Illinois Realtors and reported in Crain's, are striking. The city of Chicago went from 8,350 homes on the market in March 2019 to 2,981 in March 2026. The full Chicago metro area dropped from 32,732 to 10,456. By either measure, we are operating with roughly one third of the inventory we had in 2019, the last spring market before the pandemic and the rate driven shifts that followed.

This is not a cyclical inventory dip. The drop has been persistent for over five years, driven by structural factors that are not reversing soon. For Chicagoland real estate investors who already own rental property, that creates the most asymmetric operating environment we have seen in over a decade. This article walks through what the inventory shift specifically means for investors, the five asymmetric advantages low inventory creates, the honest flip side worth acknowledging, and what the right response looks like for owners trying to operate well here.

Key Takeaways

Chicago had 2,981 homes on the market in March 2026, compared to 8,350 in March 2019. The full Chicago metro area is down from 32,732 to 10,456. That is approximately one third of pre 2020 inventory levels.

The drop is structural, not cyclical, driven by mortgage rate lock in, slow new construction, and a generation of would be buyers priced out of the entry market. It is unlikely to reverse soon.

For existing rental property owners, low inventory creates five compounding advantages: persistent rent pressure, passive appreciation, easier tenant retention, a strong conversion opportunity for homeowners considering renting instead of selling, and a moat against out of state institutional money trying to scale Chicagoland portfolios.

The flip side is real and worth acknowledging. Renters get squeezed by rising prices, and a whole generation of first time buyers gets locked out of neighborhoods they grew up in. These outcomes are not nothing.

The right response from owners operating in this market is to lean into the responsibility that comes with the advantage. Treat tenants fairly, keep properties in good condition, and operate at a higher standard than the market is technically requiring.

Already self managing a Chicagoland rental property? Visit our free Self Managing Resource Center → for the guides, checklists, and ordinance summaries built to help owners operate well in this specific market.

How Rare This Actually Is

For some context on what is happening in Chicagoland, here is what inventory looks like in a couple of other large US markets right now.

Houston, a metro of comparable size to Chicagoland by population, had approximately 34,898 active home listings in March 2026, according to the Houston Association of Realtors. That is more than three times what the entire Chicago metro area has right now. Houston has fully recovered to pre pandemic inventory levels and is operating in what looks like a normal balanced market. Chicagoland is not.

Philadelphia is closer to Chicago's reality. The Philadelphia metro had roughly 9,095 active listings in February 2026 according to Realtor.com data, similar to Chicago's 10,456 but still around 40 percent below pre pandemic norms. Both Chicago and Philadelphia are Northeast and Midwest markets dealing with older housing stock, sluggish new construction, and significant mortgage rate lock in. They are sharing the same structural pressures.

The takeaway: Chicago's inventory drop is not a national phenomenon happening evenly across every market. It is concentrated in markets like ours, and Chicagoland is one of the more severely affected. Some of that is the regulatory and tax environment that slows new construction here. Some of it is that we have a lot of homeowners with low rate mortgages from 2020 and 2021 who are not motivated to sell. Some of it is that the entry buyer market priced out faster in metros where prices were already elevated. All of those drivers are likely to persist.

Markets like ours do not produce environments this asymmetric very often, and they do not last forever. The investors who understand what this is and operate accordingly will look back on these years as some of their best work.

What Drove the Drop

The drivers behind Chicago's inventory drop are structural rather than cyclical. Three major factors stack on top of each other.

Mortgage rate lock in. Homeowners who refinanced or bought between 2019 and 2022 locked in mortgage rates between 2.5 and 3.5 percent. Today's rates are roughly double that. Selling the property and replacing it means trading a low rate mortgage for one that costs nearly twice as much per month. Many homeowners simply refuse to make that trade, and that is keeping listings off the market.

Slow new construction. Permit activity has not kept pace with demographic demand in Chicagoland since the 2008 crash, and the gap has widened. New supply is not landing fast enough to compensate for the low resale supply.

Affordability driven exit from the entry buyer market. A whole generation of would be first time buyers cannot afford to enter the market at current prices and rates. They are renting longer, which keeps existing rental units occupied and pushes up rent on the available inventory.

None of these drivers reverse quickly. Mortgage rate lock in only resolves if rates drop substantially or homeowners are forced to sell for life events. New construction takes years to scale. Affordability returns either through price drops or significant wage growth, neither of which is imminent. The honest read is that inventory stays tight for the foreseeable future.

1. Rents Are Not Going Down Anytime Soon

The simplest way to understand the rental rate dynamic in this market: rent is downstream from housing supply. When fewer homes are available for purchase, more people stay in the rental market longer, demand for rental units intensifies, and rents rise.

This is happening across most of Chicagoland. Even in neighborhoods where rents had been flat or modestly growing through 2022 and 2023, we have seen accelerating rent growth through 2024, 2025, and into 2026. Renewal increases that would have felt aggressive five years ago are now in the normal range.

I was curious to see what this actually looks like on the rental side, so I jumped into the MLS this week. Across all of Chicago, there are only 25 active rental listings priced under $1,000. Expand the search to include listings up to $1,200 and the count only jumps to 90 across the entire city. For a city of nearly 3 million people, that is essentially zero available inventory at the price point most working class renters and entry level professionals can afford. The supply pressure is not abstract. It is concrete, it is severe, and it is one of the clearest signals that rents in Chicago are not coming down anytime soon.

For owners who already hold rental property, this is the most visible benefit of the inventory environment. It shows up directly on the monthly statement. Rent that compounds at a few percent per year over the course of a 5 to 10 year hold becomes meaningful equity even without any improvements to the property itself.

The corollary worth noting: the gap between your existing tenant's rent and current market rent may be widening. Each renewal cycle is an opportunity to bring rent closer to current market. This needs to be balanced against tenant retention (more on that below), but the gap is real and worth analyzing every renewal.

2. Your Property Is Appreciating Passively

Real estate values are partly a function of comparable sales. When fewer comparable properties hit the market, the ones that do sell tend to clear at higher prices. Bidding wars compress price discovery into the highest motivated buyer, which becomes the new benchmark for the next sale.

The result: your property gained equity in 2024, 2025, and into 2026 without you doing anything. Same square footage. Same neighborhood. Same condition. Higher value because the comps repriced upward.

This compounds across multiple years. The passive appreciation on a Chicagoland rental property held through this period adds meaningfully to total return when combined with the rent growth above. Investors who held through 2019 to 2026 typically have meaningful equity gains that are not reflected on their property tax assessments yet but are very real on a refinance or sale.

That last point is worth flagging on its own. With more equity in the property, the refinance optionality has expanded. Owners can pull capital out of one property to acquire the next without having to sell anything, which compounds the portfolio strategy faster than it would in a flat or declining market.

3. Tenant Retention Got Easier

Here is one of the less obvious benefits of low inventory: tenants are renewing at higher rates because their alternatives shrank.

Five years ago, a tenant who got a renewal letter could realistically shop around within their neighborhood and find five to ten comparable units to consider. Today, the same tenant might find two or three comparable units, often at meaningfully higher rents than the renewal offer in front of them. The math of moving (security deposit, moving costs, time off work, the unknown of a new building) gets harder to justify when the market alternative is not clearly better.

For property owners, this shows up in three ways. Higher renewal rates, which means lower vacancy across the portfolio. Lower turnover frequency, which means lower turnover costs (cleaning, paint, lock changes, leasing fees, vacancy gaps). And less leasing activity overall, which means less time and energy spent on the screening, showing, and onboarding cycle.

The math is significant. A tenant who renews for one additional year instead of moving saves the property owner roughly one month of vacancy plus two to four thousand dollars in turnover and leasing costs. Multiply that by every renewal in the portfolio and the savings stack quickly.

Want the deeper Chicagoland landlord playbook? Download our free ebook → for a more thorough guide to operating rental property in this market than any single article can cover.

4. The Conversion Play Is the Play

For homeowners considering selling their current property, the math in 2026 increasingly favors renting it out instead. This is what we have started calling the conversion play, and it deserves its own section because it is one of the most underutilized strategies in this market.

The logic: if you sell, you cash out at the current price (which is elevated by low inventory) but you lose the future appreciation and you owe transaction costs (typically 6 percent of sale price between commissions and closing costs). If you rent the property out, you keep the asset, capture continuing appreciation, capture elevated rental income, and defer transaction costs indefinitely. As long as the property can carry itself at current rent (which is more likely than ever given how rents have moved), the conversion is the better strategy for many owners.

This is especially powerful for owners who acquired the property at a low cost basis and have significant equity. The property produces income while the value continues to climb. The owner captures the appreciation without giving up control of the asset to a new buyer.

The reasons not to do this are real and worth being honest about. The owner becomes a landlord, which is a different operating reality than being a homeowner. Maintenance, tenant management, compliance with the CRLTO or CCRTLO, vacancy risk, and a different tax treatment all come with it. But for an owner who is willing to learn or to outsource the operational side, the conversion play in this market is one of the strongest wealth building moves available right now. We have walked through the conversion process in more depth here.

5. Local Operators Have a Moat Against Institutional Money

One of the underappreciated effects of low inventory is what it does to institutional buyers.

Institutional real estate operators (private equity, REITs, large national property management firms) need volume to make their economics work. They need to acquire dozens or hundreds of properties in a region to justify the operational infrastructure they bring. When inventory is abundant, they can build that portfolio relatively quickly through aggressive market participation. When inventory is constrained, they cannot.

Today's Chicagoland inventory environment is structurally hostile to institutional accumulation. The listings just are not there. The properties that do come on the market often get tied up in local bidding activity that institutional buyers cannot easily win without overpaying. The result is that local operators have a moat that did not exist five years ago.

This benefits Chicagoland investors who already own. The competition for the next acquisition is largely other local investors, not national platforms with cheaper cost of capital. The competition for tenants is similarly local. The advantage compounds over time because it gives existing owners more room to build positions in specific neighborhoods without being out competed by buyers with structurally different economics.

The Honest Flip Side

Everything above is true and good for existing rental property owners. It is also worth acknowledging that the same conditions create real hardship for two groups of people.

Renters get squeezed. Higher prices on the for sale side push rents up, but they do not push wages up at the same rate. A growing portion of Chicagoland's rental population is spending an uncomfortable percentage of income on housing. This is a real problem for the people living in our properties, and it is not getting better.

A generation of first time buyers is getting locked out. People who would have bought their first home at 28 or 30 in a normal market are still renting at 35 or 38. Some are simply unable to assemble the down payment in an environment where prices keep moving away from them. Others are unable to qualify at current rates. Many will rent for years longer than they expected, and some may rent permanently in neighborhoods where their parents would have bought.

These outcomes are not the fault of any individual investor. They are the macro result of a complex housing supply and finance system. But they are real, and investors who profit from this market should at least be honest with themselves about what is happening to everyone else.

The Bottom Line

For Chicagoland real estate investors who already own rental property, the inventory environment of 2026 is the most asymmetric operating environment in over a decade. Rents are growing. Property values are appreciating passively. Tenants are renewing at higher rates. The conversion play is the strongest it has been. And the moat against institutional capital is real.

None of that changes the math for the people on the other side of this market, who are facing real and worsening affordability problems. That is the honest tension worth acknowledging.

What the inventory shift does change for investors is the responsibility that comes with the advantage. If you own a rental property in Chicagoland and you are operating in this market, the bar for what good operation looks like has gotten higher. Treat your tenants fairly. Keep your properties in genuinely good condition. Resolve maintenance promptly. Respond to issues without dragging your feet. Be the kind of landlord this market needs more of.

The opportunity in this market is real, but it is not free. It comes with a higher standard of operation, and the investors who meet that standard will be the ones who do well in this environment over the long run.

The owners I see operating most successfully in this environment are not the ones with the most aggressive rent strategies or the lowest cost vendors. They are the ones who understood that the asymmetric advantage of this market is also a chance to set a higher standard for how rental property gets operated in Chicago. The math is good. The responsibility is real. Both can be true.

Frequently Asked Questions About Chicago's Inventory Environment

Will the Chicago inventory situation reverse soon?

Unlikely. The drivers (mortgage rate lock in, slow new construction, affordability driven exit from the entry buyer market) are structural rather than cyclical. They could reverse if mortgage rates drop substantially, new construction accelerates dramatically, or prices fall enough to bring entry level buyers back. None of those seems imminent, but the market can always surprise. The honest read for the next 12 to 24 months is that inventory stays tight.

Should I sell my Chicagoland rental property to capture the elevated prices?

Probably not, but it depends on your specific situation. The case for selling is that you can lock in current prices and exit. The case against is that you lose continuing rent growth, ongoing appreciation, and the tax treatment of holding. For most investors with healthy cash flow and a long term horizon, holding outperforms selling in this market. The exceptions are if your property has structural problems that make holding genuinely difficult, or if you have a 1031 exchange opportunity that meaningfully improves your position.

Is now a good time to acquire more Chicagoland rental property?

It is a harder time to acquire than it was five years ago because there is less inventory and prices are elevated. But the underlying economics on a property you can acquire and operate well remain strong. The key is being disciplined about the acquisition price (do not overpay just because you want a property), the underwriting (use realistic maintenance reserves, rent assumptions, and turnover expectations), and the operational plan.

How should I think about renewal rent increases in this market?

Renewal rent decisions should balance current market rent against tenant retention. The gap between in place rent and market rent has widened for many properties, so a meaningful increase at renewal is often justified. But pushing too aggressively can trigger a turnover that costs more than the increase captures. The right answer depends on the specific property, the specific tenant, and your overall strategy on holding versus repositioning.

What should I do if I am a homeowner considering whether to sell or rent?

In a low inventory market with rising rents and appreciating values, the conversion play (renting your property instead of selling it) is often the stronger move. The math depends on your cost basis, your current mortgage rate, the rent the property can command, and your willingness to operate as a landlord. A property management firm can model this for you in 30 minutes, and many homeowners discover that converting is meaningfully better than selling.

Don't Go At This Alone!

At GC Realty & Development, we manage approximately 1,500 units across Chicagoland with a fully staffed in house team handling maintenance, leasing, compliance, and accounting under one roof. We are seeing the inventory shift play out across our entire portfolio in real time, and we are helping owners think through what it means for their specific properties.

If you own a Chicagoland rental and want a second set of eyes on what your property is worth in this market, what your rent should be, or whether the conversion play makes sense for a property you are considering renting instead of selling, we are happy to walk through it with you.

Mark's Mission: My personal mission is to help property owners across Chicagoland keep more of their time, more of their money, and less of the risk that comes with running rentals in one of the most regulated markets in the country.