Vendor Portal

Vendor Portal

Author: Mark Ainely | Partner GC Realty & Development & Co-Host Straight Up Chicago Investor Podcast

Chicago real estate investors have long heralded the importance of cash flow from rental properties. Unfortunately, too many landlords focus just on the cash flow aspect alone.

This can cause them to snap up properties that look like great cash cows but end up having problems that require paying out of pocket to solve. Others sit on the sidelines waiting the unicorn cash flowing purchases to fall into their laps. Both groups end up missing out on tons of opportunities by only focusing on cash flow instead of looking at the bigger picture. How’d we get here?

What Is Cash Flow?

Before buying any investment property, owners need to determine if they’ll receive a good return on their investment (ROI). One way to determine ROI is to estimate a property’s cash flow value.

Cash flow is the money earned from a rental property. You calculate cash flow by subtracting expenses (like maintenance, utilities, taxes, cleaning and loan payments) from rental income (aka “the rent money”). The remaining amount is the cash flow. A property can have negative or positive cash flow, which also changes over time as income and expenses fluctuate.

Chasing Financial Freedom through Real Estate Investing

Buy-and-hold real estate investors build wealth in multiple ways. Cash flow is just one of these ways. We hear more about cash flow because it’s the sexiest, most talked about aspect because of all the hype around attaining “financial freedom.”

Cash flow also feeds our need for instant gratification. But I’m going to bust your bubble early here! Overnight successes rarely happen overnight.

Unless you actively raise money and buy millions of dollars worth of property right out the gate, don’t expect that financial freedom overnight. Don’t even expect it within the first decade of your real estate investing career.

Financial Freedom Beyond Cash Flow

When investors focus too heavily on cash flow, they neglect the other important ways to use real estate to build wealth. Of course, positive cash flow is ideal, but even if you break even or lose a bit, you can still build wealth from the same property. By looking beyond cash flow, investors will find that financial freedom isn’t as elusive (albeit not as sexy) as those unicorn cash flowing properties.

Our Chicago property management company has shown hundreds of clients how to build the type of wealth that ultimately leads to financial freedom. We’ve helped Chicago landlords learn how to maximize all five lucrative revenue streams their rental properties provide.

You can tap into these five profit sources, too, even from a just single rental property. Here's how:

How Principal Paydown Builds Wealth

Mortgage payments cover principal, interest, taxes, and insurance. Just like in your primary home, principal builds wealth by reducing your loan balance while your property appreciates. On a rental home, you essentially pay rent to yourself.

For example, say you buy a $250k property with a $240k loan. After 30 years, you'll owe $0 and own a $250k asset (which appreciated to even more than that original value). You turn a small down payment ($10k) into an asset.

Of course, it doesn’t have have to take you 30 years to get here. You can use a variety of strategies to pay off the loan faster (and ultimately saving thousands on interest payments), including:

Pay extra each month – Every time you pay even a few dollars over the minimium payment dues, that amount comes directly off the principal. For example, on a $500k loan at 7.5%:

An extra $100 per month = 33 months quicker pay off / $185,441.31 less in interest

An extra $291 per month = 77 months quicker pay off / $191,196.40 less in interest (extra payment)

Make bi-weekly payments – Whatever your monthly mortgage payment is, pay half of it every two weeks. That ends up being 26 half-payments in a 52-week year. So, you end up making 13 monthly payments instead of just 12.

Remit one additional payment annually – Getting a nice tax return? Use a portion of it to make an extra payment.

Income Tax Liability Reduced

Real estate investors can reduce what they legally have to pay Uncle Sam in federal taxes each year just by owning rental property! When used right, can get you a refund back when you should have owed money. At the very least it will provide you a substanial reduction in tax liability.

As a rental property owner, you can deduct certain expenses on your tax return from rental income. These include mortgage interest, property taxes, operating expenses, depreciation, and repairs.

You also can deduct necessary expenses for managing your property. These include leasing commissions, maintenance, utilities, management fees, and insurance.

Can I Reduce My Income Tax Liability By Investing?

You can most certainly reduce your tax liability through investing in rental properties. Anyone can, especially here in Chicago.

Take a $300k rental property purchase with a 95% loan-to-value ratio and 7.25% interest rate. An investor with a W2 income of $100k can benefit from not paying approximately $4,200 of income and state tax here in Illinois.

ALWAYS, talk to your CPA about deductions and what makes sense for your situation. In general, large expenses can help your taxes over time. The IRS offers guidelines; however, your CPA can ensure you claim deductions effectively and correctly.

Reducing Tax Liability For Chicago Investors

We cover a lot more on this topic on our podcast, Straight Up Chicago Investor. We’ve done a lot of the research and talked to the experts on tax strategies. So check out our guest, one of the top accountant/financial planners in Chicago, and consider reaching out to him to learn more.

Hedge Against Inflation

Did you purchase or refinance a mortgage in 2017-2022? How much do you love that 2.5-3.5% interest rate you recieved for a 30-year loan? Congratulations! You have the most to gain in our current economic environment.

Economic uncertainties and inflation can affect your finances. However, owning rental property provides a buffer. Rental income typically increases with market demand and inflation rates. With a fixed-interest loan, your mortgage payments remain stable. But, rising rent boosts your cash flow.

Even with high interest rates, carefully assessing rent rates can yield favorable returns. When interest rates drop, refinancing can further enhance your returns.

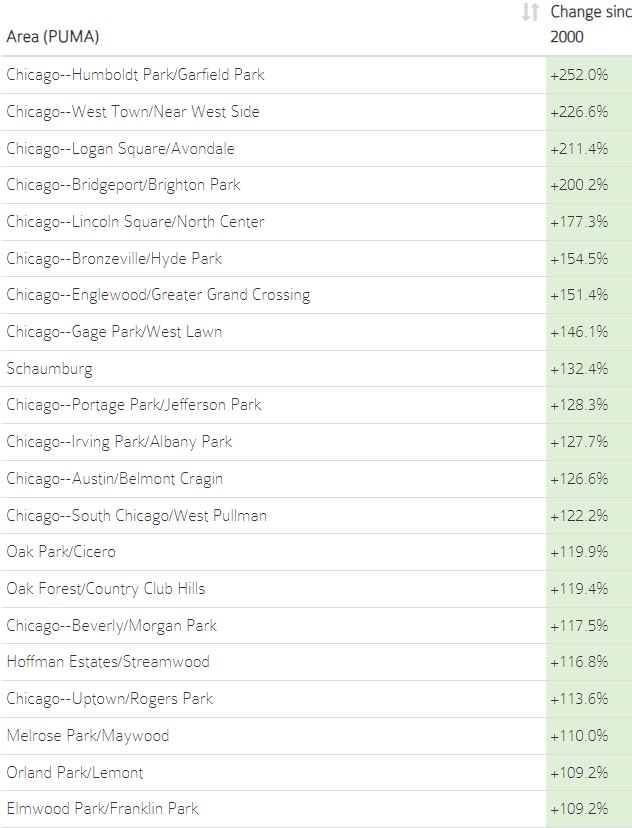

Property Appreciation

Property appreciation, the final wealth driver, boosted sellers and landlords during the pandemic. Housing prices surged, then stabilized at higher levels post-pandemic.

A well-kept property usually gains value over time. By reducing your loan amouhnt, you gain equity. This equity grows with property value hikes. Choosing properties wisely and maintaining them boosts their value.

Time Is Your Greatest Asset

Caution: more bubble-bursting ahead! The truth is time is your greatest asset. By buying one property today, in 10 years, you’ll have a great asset that provides you with:

Equity – You’ll gain considerable equity from paying down the principal balance. Even if you don’t may any extra payments, depending on your initial down payment, you could have 30-50% equity available in your investment.

Tax Savings – After realizing 10 years’ worth of income tax benefits, you’ll have kept thousands of extra dollars in your pocket. That’s cash you don’t have to pay Uncle Sam.

F*%k Inflation – Even if you have 6-8% interest rate, you’re leveraging a lot of money at a fixed rate for 30 years. D*mn, that feels good, doesn’t it?

Property Appreciation – Outside of blips in pricing, during any 10-year period, you find home values go up year-to-year. We appreciate home property appreciation because it sneaks up on you (in a good way).

Why Aren’t You Buying Your Next Chicagoland Property Now?

They say the best time to plant a tree is 20 years ago, and the next best time is today. After 20 years of investing myself (mostly here in the Chicago market), I still wish I would’ve planted more trees 20 years ago. At the same time, I wish I never would’ve sold a lot of the properties I did, for the same reasons.

I better understand now what I didn’t at the time: by not investing in real estate, you’re losing wealth. If you still find yourself sitting on the sidelines waiting for something (an invitation? the perfect cash flow unicorn? to win the lottery?), you, my friend, are losing money.

The longer your cash sits in your bank account earning less than 5%, the more equity you lose by not investing in rental property. We all hear about inflation, but it effects the value of your cash hanging out with you on the sidelines. You may as well stuff the cash in your mattress like your grandparents.

Get A Broker and Get After It

Done sitting around watching other people get rich? Stop chasing cash flow dreams and look at the bigger picture for growing wealth. An investment property broker can help. If you need a referral for a broker, schedule a call below.

If you’re a licensed real estate broker, still schedule a call and we can advise you as well. We might hit you up for property management referrals. But we pay referral fees for those in addition to the free advice we can provide for you and your clients.

Where to Start?

Download the first part of our two-part series, Where to Invest in Chicago - Suburb Edition. You’ll benefit from 20 years of learning the Greater Chicago rental property market and how to find the hidden gems. Just as importantly, we share tips on when to run away from a deal, no matter how sexy it looks on paper.

Get the secrets and save money Get the secrets and save money |  📅Schedule a call with an expert 📅Schedule a call with an expert |